News & Resources

Coronavirus Aid, Recovery, and Economic Security (CARES) Act

Act")

March 28, 2020 update:

-

Relief Payments to Individuals

-

Business and Individual Taxation Considerations

-

Other Opportunities Under the CARES Act

-

Retirement Plan Distributions

March 27, 2020 update:

March 26, 2020:

-

A third round of COVID-19 Relief

-

Update on Families First Coronavirus Response Act FMLA Provisions

-

Client Update from WK

Updated Saturday, March 28, 2020 –

Relief Payments to Individuals

Stimulus Payments To Provide Relief Under CARES Act

The Coronavirus Aid, Relief, and Economic Security (CARES) Act provides recovery rebates to eligible individuals, issued as checks or direct deposit payments. The payment dates are unclear at this time, and WK will provide clarification when definitive information is available. These recovery rebates are treated as advance refunds of a 2020 tax credit.

To follow is a summary of the rules related to the advance refunds.

Recovery rebate amounts

- $1,200 per eligible individual tax filers ($2,400 for eligible joint filers)

- Plus: $500 multiplied by the number of qualifying children (dependents under age 17)

Income Limitations

The recovery rebate shall be reduced by 5% when adjusted gross income (AGI) exceeds the following thresholds.

- $150,000 in the case of a joint return

- $112,500 in the case of individual head of household

- $75,000 single and married filing separate

How Recovery Rebate Amounts Are Determined

The United States Treasury will use the following factors to determine the amount of each advanced payment.

- Adjusted gross income reported on your 2019 federal income tax return (if filed)

- Adjusted gross income reported on your 2018 federal income tax return if your 2019 return has not been filed

- Social Security benefit statement if not required to file a federal income tax return for 2018 or 2019

Note: If it is determined at a later date by review of 2020 federal income tax return that your advanced payment was too large, you will not be required to repay the credit.

Ineligible Individuals

- Any nonresident alien

- Individuals who can be claimed as a dependent by another taxpayer

- An estate or trust

Delivery Method

- Direct Deposit if on file

- Mailed to your home, if not using Direct Deposit

Business and Individual Taxation Considerations

If I have a horrible year, is relief available?

Ability to Claim NOL Carrybacks and Enhanced Carryforwards

The Coronavirus Aid, Recovery, and Economic Security (CARES) Act relaxes the limitations on a company’s use of losses. As part of the Tax Cuts and Jobs Act (TCJA), carrybacks of net operating losses (NOL) were disallowed (using NOLs to reduce income in a prior tax year were disallowed by TCJA) and NOLs incurred after 2017 that were carried forward were limited to 80% of taxable income.

The CARES Act allows NOLs occurring in a tax year beginning in 2018, 2019 or 2020 to be carried back five years, and losses carried to 2019 and 2020 may be used to offset 100% of taxable income, as opposed to 80% under TCJA. These changes will allow companies to utilize losses and amend prior year returns.

For example: Company A broke even in 2015 and 2016 (taxable income was $0). In 2017, Company A had $1 million of taxable income and paid $350,000 in federal income taxes. Company A had $2 million of taxable income in 2018 and paid $420,000 in taxes. Because of the coronavirus’ detrimental effects on the global economy, Company A generated a $3 million net operating loss (NOL).

In this example, Company A may carry $1 million of the loss back to 2017 and recover the $340,000 of federal income taxes paid (subject to the alternative minimum tax). It may also carry the remaining $2 million NOL to 2018 and recover the $420,000 of federal income taxes paid in that year as well.

Real Estate Investment Trusts (REITs) cannot carryback NOLs to any tax year, and NOLs of a taxpayer may not be carried back to any year in which the taxpayer met the definition of a REIT.

Temporary (and Retroactive) Removal of the 4th Limitation on Losses for Individuals

As part of TCJA, total losses from all of an individual taxpayer’s trades or businesses were limited to the amount of income earned from those businesses plus $250,000 ($500,000 for joint returns). Any excess loss was converted into an NOL.

The CARES Act eliminates this loss limitation for tax years 2018, 2019 and 2020. As a result, taxpayers who had losses limited by this new provision of the TCJA in 2018 or 2019 can file an amended return to claim a refund. An unfortunate aspect of the CARES Act is the clarification that when the excess business losses provision of the TCJA (the 4th limitation on losses) goes back into effect in 2021, wages will not be considered business income.

Acceleration of Credits for Prior Year Minimum Tax Liability of Corporations

TCJA repealed the corporate alternative minimum tax (AMT), but corporate AMT credits were made available as refundable credits over several years, ending in 2021. Under TCJA, any remaining AMT credits in 2021 would be 100% refundable. However, the CARES Act allows any remaining AMT credits to be 100% refundable in 2019.

The CARES Act Temporarily Increases the Amount of Interest Businesses May Deduct

TCJA limited the amount of interest expense a business may deduct to the sum of (1) the business’ interest income, (2) 30% of “adjusted taxable income” (taxable income with some adjustments), and (3) floor plan financing interest.

For 2019 and 2020, the CARES Act temporarily increases the amount of interest expense businesses are allowed to deduct on their tax returns to 50 percent of “adjusted taxable income,” up from 30 percent. This temporarily reduces the cost of capital for businesses.

Because most businesses won’t have taxable income for 2020, the CARES Act allows businesses to elect to use its 2019 taxable income for purposes of computing the 2020 limitation on deducting interest expense. As an example, if Business A’s “adjusted taxable income” for 2019 and 2020 was $8 million and $0, respectively, the business can elect to deduct $4 million of interest expense in 2020, generate a larger NOL for 2020, and then carry back the loss to 2019 and get a refund (NOL carrybacks are temporarily allowed again as part of the CARES Act).

Partnerships, however, don’t get an increase in the percentage of interest expense they can deduct in 2019, but 50% of the suspended interest that is allocated to partners for 2019 will be deductible by the partners in 2020 without being subject to the limitations on deducting business interest expense, and the other 50% will continue to be suspended until the partner is allocated enough interest income or taxable income.

It is important to remember that the limitation on the deductibility of interest expense that was passed as part of TCJA does not apply to “small business taxpayers,” businesses with average annual gross receipts for the three-year annual period ending with the prior tax year of $25 million or less (indexed for inflation).

Other Opportunities Under the CARES Act

Qualified Improvement Property is now Eligible for Bonus Depreciation

Congress intended to make Qualified Improvement Property (QIP) eligible for bonus depreciation as part of TCJA but failed to do so by forgetting to reduce the depreciable life of QIP to 15 years from 39 years (bonus depreciation is available for all assets with a depreciable life of 20 years or less).

The CARES Act reduced the depreciable life of qualified improvement property from 39 years to 15 years, thus making it eligible for bonus depreciation. Bonus depreciation allows a taxpayer to fully deduct eligible property. As an example, a taxpayer spent $1 million renovating a restaurant in 2018. Prior to the CARES Act, the taxpayer had to depreciate the $1 million over 39 years, but the CARES Act allows the taxpayer to fully deduct the $1 million in 2018 by filing an amended return. If the taxpayer deducted $25,000 in 2018, he or she may file an amended return to take an additional deduction of $975,000. To the extent any net operating loss is generated by the additional depreciation, the NOL may be carried back for up to five years to recover taxes previously paid.

$300 Above-the-Line Deduction for Charitable Contributions

In order for a taxpayer to claim a deduction for charitable contributions, the taxpayer must itemize as opposed to taking the standard deduction. However, the CARES Act encourages Americans to contribute to charitable organizations in 2020 by permitting them to deduct up to $300 of cash contributions on their 2020 tax return, whether they itemize their deductions or not. This is similar to an “above-the-line” deduction, such as student loan interest.

Percentage Limitations on the Deduction for Charitable Contributions Increased

The CARES Act increases the limitations on deductions for charitable contributions by individuals who itemize, as well as corporations.

For individuals, the 50% of adjusted gross income limitation is suspended for 2020. This allows individuals to deduct up to 100% of their AGI for 2020, with any excess contributions available to be carried over to the next five years. For corporations, the 10% limitation is increased to 25% of taxable income.

The CARES Act also increases the limitation on deductions for contributions of food inventory from 15%to 25%.

Retirement Plan Distributions

Retirement Plan Relief

Various provisions are included in the CARES Act with regard to retirement plans, including the following items:

- The 10% early withdrawal penalty tax will be waived for coronavirus-related hardship distributions up to $100,000. This waiver applies under the following conditions:

- Individuals diagnosed with COVID-19 by a test approved by Centers of Disease Control;

- Individuals whose spouse or dependent is diagnosed with COVID-19 by such test;

- Individuals who experience adverse financial consequences as a result of being quarantined, furloughed, laid off, having reduced work hours, unable to work due to lack of child care due to COVID-19, closing or reducing hours of a business owned or operated by the individual due to COVID-19; or

- Other factors as determined by the Secretary of the Treasury.

- Individuals can pay tax income taxes on these hardship distributions ratably over a three-year period. These distributions can also be repaid to a plan within 3 years to avoid taxation. Such repayments are not subject to the plan’s contribution limits.

- Qualified plan loan limits have increased to the lesser of $100,000 or 100% of the vested balance of the account from previous limits of $50,000 or 50% of the vested balance for individuals meeting the coronavirus-related conditions above.

- Participants meeting the coronavirus-related conditions with outstanding plan loans may delay repayment due dates scheduled through December 31, 2020 for a year.

- Provisions have been included to allow plan providers to follow these new rules before they have had a chance to amend their plan documents, provided the plan is amended on or before the last day of the plan year.

- A temporary waiver of required minimum distributions for 2020 for defined contribution plans and IRA’s.

As always, the rules related to retirement plans are very specific to the plan type, and your situation and can have long lasting impacts on your retirement savings. Always consult with both your tax advisor and your investment advisor before making retirement plan decisions to ensure all options have been considered.

Additional information about the impact of COVID-19 will be provided as the situation develops. We will communicate those alerts via email and on our website at https://williamskeepers.com/covid-19-resource-center/.

Updated Friday, March 27, 2020 –

Employer Payroll Taxes

The United States Treasury has yet to issue guidance on the specifics of how the credits for expanded paid sick and childcare leave will be administered. See our prior article regarding the leave requirements.

The credit is designed to offset payroll taxes immediately, and guidance will be issued on how to claim accelerated payments of the credit to the extent an employer’s total credit exceeds their total payroll taxes required to be remitted for all employees.

The Internal Revenue Service provided these examples

If an eligible employer paid $5,000 in sick leave and is otherwise required to deposit $8,000 in payroll taxes, including taxes withheld from all its employees, the employer could use up to $5,000 of the $8,000 of taxes it was going to deposit for making qualified leave payments. The employer would only be required under the law to deposit the remaining $3,000 on its next regular deposit date.

If an eligible employer paid $10,000 in sick leave and was required to deposit $8,000 in taxes, the employer could use the entire $8,000 of taxes in order to make qualified leave payments and file a request for an accelerated credit for the remaining $2,000.

The credit is also going to cover the costs to maintain health insurance coverage for employees on eligible leave. More guidance should follow.

There will also to be a credit for self-employed individuals in similar situations. More guidance for self-employed individuals and accelerated payment of this credit is expected.

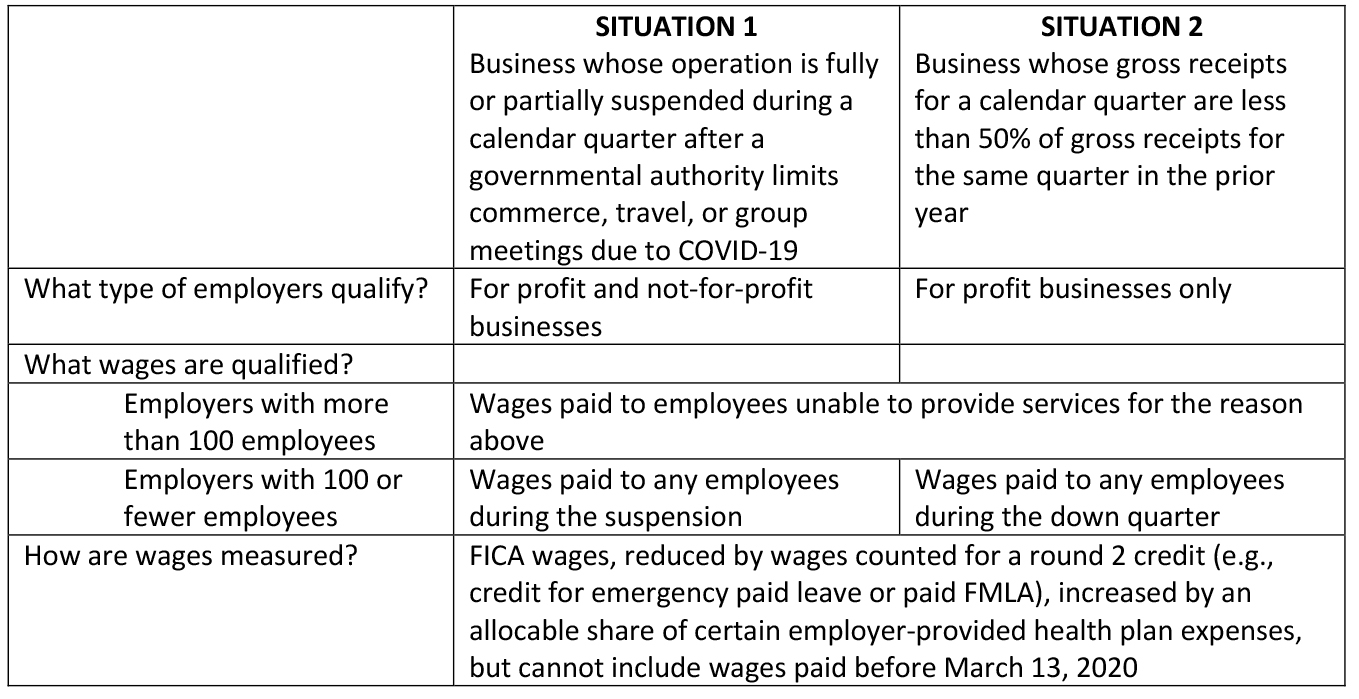

Employee Retention Tax Credits

In Round 2 of its legislative response to COVID-19, the United States Congress included an incentive to help small businesses continue to maintain their payroll by offering a credit to defray in whole or part wages paid to employees missing work as a result of specified COVID-19 events and paid FMLA to employees who left their jobs to care for children due to school or child-care facility closures.

The Round 2 incentives were not targeted to help businesses generally affected by financial strain imposed by community business suspensions or significant reductions in demand.

Round 3 of legislation approved by Congress and signed into law by President Donald Trump on March 27, 2020 includes a federal subsidy capped at $5,000 per employee. That cap will be administered through a refundable payroll tax credit, calculated based on 50% of qualified wages paid to employees in either of the following two situations.

Certain affiliated businesses will be unable to claim the credit in each business. Also, employers who receive an SBA small business interruption loan cannot claim the credit.

The credit offsets the business’s OASDI payroll tax liability. However, if the credit exceeds the quarterly liability, the excess produces a refundable credit.

Paycheck Protection Program (PPP)

A major component of the CARES Act is the Payroll Protection Program, designed to encourage businesses to maintain current levels of employment while providing access to funds to aid in the payment of payroll and overhead costs during these difficult times.

Under the Payroll Protection Program, a business with 500 or fewer employees (“eligible business”) can apply for an SBA loan (“covered loan”) equal to 2.5 times the business’s average monthly payroll costs for the prior 12 months (up to a maximum loan of $10 million). Payroll costs include payments for salaries, wages, commissions, tips, certain covered benefits, state and local tax assessed on compensation, and compensation to or income of a sole proprietor or independent contractor (but only on net self-employment earnings or similar compensation of less than $100,000 in one year). Specifically excluded payroll costs include compensation above $100,000 per employee, payroll taxes, and emergency sick leave or expanded FMLA paid leave subject to tax credits under the Families First Coronavirus Response Act (see here for information on these credits).

Allowable uses of the proceeds of covered loans are:

- payroll costs;

- costs related to continuation of group health care benefits during periods of paid sick, medical, or family leave, and insurance premiums;

- employee salaries, commissions, or similar compensations;

- mortgage interest;

- rent;

- utilities;

- interest on other debt obligations incurred before February 15, 2020.

An eligible business must make a good faith certification that the uncertainty of current economic conditions makes necessary the loan request to support the ongoing operations of the eligible recipient, as well as acknowledge that funds will be used to retain workers and maintain payroll, or to make mortgage payments, lease payments, and utility payments.

Any portion of the loan that is not forgiven (see below) will have a maximum maturity of 10 years at an interest rate not to exceed 4%. During the period beginning on February 15, 2020 and ending on June 30, 2020, lenders are required to provide complete payment deferment for at least six months and up to one year.

As stated above, the program does allow for forgiveness of indebtedness on a covered loan in an amount paid for the following items during the 8-week period beginning on the date of origination of the covered loan:

- payroll costs;

- interest on mortgage indebtedness incurred before February 15, 2020;

- rent obligations on lease agreements in force before February 15, 2020;

- utility payments for services, for which service began before February 15, 2020.

The amount of loan forgiveness will be reduced, however, if either of the following occurs during the eight week period following the origination date of the covered loan:

- the average number of full-time equivalent employees for the eight week period is less than the average number of full-time equivalent employees during the baseline period (either 2/15/19 – 6/30/19 or 1/1/20 – 2/29/20); or

- there is a more than 25% reduction in the wages of a non-highly compensated employee (an employee who, during 2019, did not have an annualized rate of pay of more than $100,000 during any single pay period).

If, however, within 30 days of the enactment of the CARES Act there is either a reduction in number of employees or a reduction in employee wages (as compared to number of employees and wages as of February 15, 2020), a business can rehire employees to get back to previous employment levels, or restore employee wages to previous levels, by June 30, 2020 and not experience a reduction in the amount of loan forgiveness. In other words, businesses that have let employees go or reduced wages since February 15, 2020 have the option of rehiring those employees or restoring wages to their original levels so as to not lose out on loan forgiveness.

Previous Update (Dated Thursday, March 26, 2020) –

A third round of COVID-19 relief is working its way through the United States Congress, having been passed unanimously by the Senate early today.

A vote in the House of Representatives is expected on Friday. In its current form, the Coronavirus Aid, Recovery, and Economic Security (CARES) Act will likely have a substantial impact on individuals and businesses that represent a variety of industries.

Williams-Keepers LLC has a team of experienced advisors evaluating how the legislation affects the firm’s clients and the business decisions they face. Additional information will follow once the bill has been approved and signed into law by President Donald Trump.

To read our alerts on the previous two phases of the Act and how they may impact you or your business please click here.

Update on Families First Coronavirus Response Act FMLA Provisions

The Department of Labor has issued a Q & A on the provisions of the Families First Coronavirus Response Act to help employers better understand the leave requirements of the new law. These provisions take effect on April 1, 2020 and extend through December 31, 2020. The Q & A can be found here.

You can also read more about the FMLA provisions for the Families First Coronavirus Response Act in our previous client alerts here.

Client Update from WK

WK chairman, Jeff Echelmeier, discusses Williams-Keepers LLC’s response to COVID-19 and an update to our clients in this short video.

WK greatly appreciates the patience, understanding and continued support demonstrated by all of its clients during this unprecedented, difficult time. The firm will continue to provide applicable updates using www.williamskeepers.com and email communications. To read previous updates regarding COVID-19 please click here.

Our sincere hope is that everyone remains safe in the immediate term, and we look forward to resuming normal business operations at the appropriate time.

In accordance with recommendations made earlier this week by the Boone County Health Department and several other statewide and local directives, WK has discontinued its daily open-to-the-public office hours schedule in both its Columbia and Jefferson City offices through Friday, April 24, 2020. Clients can continue to call both offices – either (573) 442-6171 (Columbia) or (573) 635-6196 (Jefferson City) – during the hours of 8:00 a.m. until 5 p.m., Monday through Friday.

To ensure its clients’ safety and compliance with these directives, the firm has discontinued the physical receipt of information in its offices. Other options for sharing information with the firm include:

- use of the firm’s client secure, website-based portal and LeapFile system for the delivery of electronic documents; and

- delivery to the firm using the United States Postal Service or another commercial delivery service.

The firm will also share information with clients using these delivery methods for the foreseeable future.

Clients who have questions about how to use the firm’s electronic document delivery systems should contact their WK advisor.